Welcome to CDP's global website

Please select the site for your country / region to view the most suitable information

In 2019, CDP released a Global Climate Change Report which explored TCFD-aligned disclosures in the 2018 reporting cycle and provided key insights into the potential financial implications of climate change. The report identified, through corporate disclosures, that the benefits of climate action far outstrip the costs of doing so, and the risks associated with inaction will be detrimental to the global economy.

Following on from CDP’s 2019 report, this series explores key G7 indexes. The series focuses on the corporates within each index that disclosed via CDP’s 2021 Climate Change Questionnaire and will not look beyond by assessing external financial filings or mainstream reports.

TCFD alignment in G7 countries: Initial insights

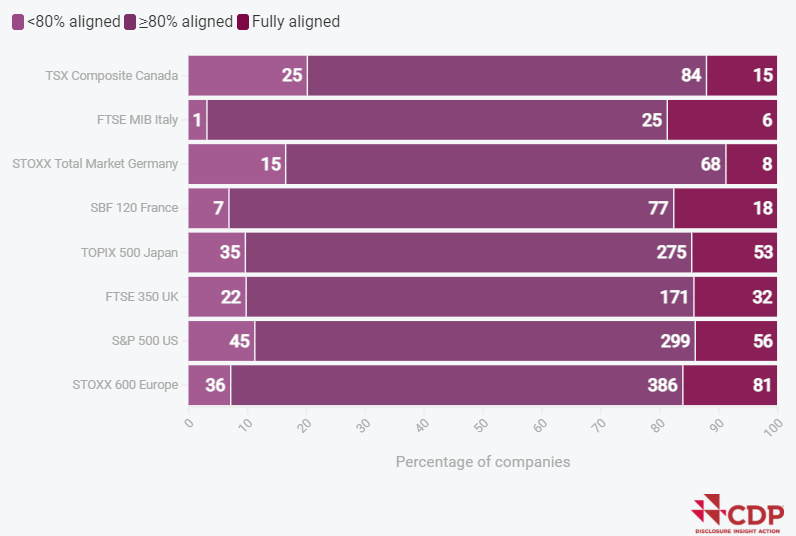

Analysis of the indexes from G7 countries and a Europe-wide Index (representing 17 European countries) reveals significant shortfalls in TCFD aligned disclosure amongst corporates. None of the indices had more than 19% of corporates achieving 100% TCFD-aligned disclosure when disclosing through CDP’s platform.

A key gap that spans across all the indices is the lack of disclosure on how climate-related information is fed into a corporate’s strategy. Companies continue to perform poorly in terms of risk management, suggesting that they do not have sufficient processes in place to assess and manage climate risk.

Read the initial insight to set the scene of how different indexes are performing against the TCFD, before a deep dive into index-specific insights.

Key findings

- CDP analysis identifies that key G7 country indices alongside a European wide index are performing relatively equally in terms of TCFD-aligned disclosure, but German and Canadian indices are lagging behind;

- No index had more than 19% of corporates achieving 100% TCFD-aligned disclosure when disclosing through CDP’s platform, identifying significant shortfalls that must be addressed;

- A key gap that spans all indices is the lack of disclosure of climate-related information and how climate is fed into a corporate’s strategy. Most notably, companies lack an understanding of climate-related scenario analysis or disclose insufficient information on their use of scenarios; and

- Companies are also performing poorly in terms of risk management, suggesting corporates do not have sufficient processes in place to identify, assess and manage climate-related risks.

In 2021, 400 companies (80%) from the S&P 500 index, worth over US$28.2 trillion in market capitalization, responded to CDP’s climate change questionnaire. This analysis explores the alignment of the disclosures with the recommendations of the TCFD and additionally provide insights into the reported financial impacts of climate-related risks and opportunities.

A landmark development in the United States is the Securities and Exchange Commission’s (SEC) announcement of its proposed climate disclosure rule. The SEC’s rule largely tracks the TCFD recommendations and S&P 500 companies providing a high-quality disclosure through CDP are well prepared for the SEC requirements. The number of CDP climate change disclosers from the index have increased about 10% over the last five years.

Key findings:

- Only 14% of the disclosing S&P 500 companies provided information on all of the TCFD-related questions.

- In aggregate, the reported financial benefits of climate-related opportunities are about 15 times higher than the potential financial impact of climate-related risks.

- The maximum financial benefits of opportunities far outweigh the costs to materialize them (aggregated across all sectors).

- While more than 80% of the disclosing companies identified climate-related risks, only 63% covered their entire value chain in their risks assessment process.

- Out of the companies that identified exposure to climate-related risks and opportunities, one-third did not provide potential financial impact estimates.

In 2021, 225 companies (64%) listed on the FTSE 350 index, representing a market capitalization of over US$2.5 trillion, responded to CDP’s climate change questionnaire. This insight piece investigates the disclosing organizations’ alignment with the recommendations of the TCFD and the reported financial impacts of climate-related risks and opportunities.

In April 2022, the UK mandated TCFD-aligned disclosure for the country’s largest traded businesses, banks, and insurers. This will help financial decision makers in understanding businesses’ financial exposure to climate-related risks through clear, comprehensive, and consistent information. Inadequate information about risks can lead to mispricing of assets and misallocation of capital that can potentially lead to concerns about the stability of financial markets and their vulnerability to abrupt corrections.

Additionally, this insight piece looked into the disclosers’ transition plans using a set of CDP indicators. This is in response to the UK government’s announcement to mandate transition plans for listed companies and financial institutions by 2023.

Key findings:

- Only 14% of the disclosing FTSE 350 companies provided information on all of the TCFD-related questions.

- In aggregate, the reported financial benefits of climate-related opportunities are twice as high as the potential financial impacts of climate-related risks.

- In aggregate, it is far less costly for businesses to manage their risks than bear the potential financial impacts of the risks materializing (US$35 billion vs. US$102 billion).

- Aggregated across all disclosures, the cost of realizing climate-related opportunities is much lower than the potential financial benefits of the opportunities (US$39.7 billion vs. US$118.6 billion).

- About half of the disclosing companies reported having developed a transition plan, however, only nine companies responded to all the key indicators of a credible climate transition plan.

In 2021, 503 companies (84%) listed on the STOXX Europe 600 index, representing a market capitalization of over US$11 trillion, responded to CDP’s climate change questionnaire. This analysis looks at the disclosing organizations’ alignment with the recommendations of the Task Force on Climate-related Financial Disclosure (TCFD) and the reported financial impacts of climate-related risks and opportunities.

Evaluating the TCFD alignment of companies listed on this European index is particularly relevant because in April 2021, the European Commission issued a proposed Corporate Sustainability Reporting Directive (CSRD). The CSRD will ensure that companies publicly disclose the climate-related risks and opportunities they face as well as the impact their business has on the environment. Company disclosures under the CSRD will need to be in line with the European Sustainability Reporting Standards (ESRS) which are being developed in alignment with existing standards and frameworks like the TCFD. Large companies are anticipated to be required to start reporting under the directive as early as 2024.

Key findings:

- Only 16% of the 503 disclosing STOXX 600 companies provided information on all of the TCFD-related questions

- The reported potential financial benefits of climate-related opportunities in aggregate are 1.5 times higher than the potential financial impacts of climate-related risks.

- In aggregate, it is less costly for businesses to manage their risks than bear the potential financial impacts of the risks materializing (~US$206 billion vs. ~US$1 trillion).

- Aggregated across sectors, the cost of realizing climate-related opportunities is much lower than the potential financial benefits of the opportunities (~US$393 billion vs. ~US$1 trillion).

In 2021, 363 companies (73%) listed on the TOPIX 500 index, representing a market capitalization of over US$4.3 trillion, responded to CDP’s climate change questionnaire. This analysis investigates the disclosing organizations’ alignment with the recommendations of the TCFD and the reported financial impacts of climate-related risks and opportunities.

Japan’s Financial Services Agency (JFSA) introduced regulations on climate disclosure in the nation’s corporate governance code in mid-2021 and the draft Revised Code was published in April 2022. Companies listed on the Prime Market segment of the Tokyo Stock Exchange, Inc. (TSE), must comply with new mandatory climate disclosure regulations. JFSA encourages the use of the TCFD framework to improve the quality and quantity of disclosure. The JFSA intends to expand its coverage to all companies that submit annual securities reports, requiring them to make necessary disclosures after fiscal year 2023.

Key findings:

- Over 90% of the companies responded to at least 80% of the TCFD-related questions in CDP's questionnaire, but only 14% of them responded to all of the TCFD indicators.

- Aggregated across the disclosing sample, the reported potential financial benefits of climate-related opportunities (US$2.9 trillion) are about 6 times higher than the potential financial impacts of climate-related risks (US$488 billion).

- Climate opportunities related to products and services were the most frequently reported, followed by opportunities related to energy source.

- For most industries, taking action to respond to climate-related risks, and investing in realizing climate opportunities, comes at a lower cost (aggregated per industry) than allowing the risks to materialize or letting the opportunities go unrealized. The exceptions are the fossil fuel and transport industries.

In 2021, 124 companies (57%) listed on the S&P TSX Composite (Canada) index, representing a market capitalization of over US$1.6 trillion, responded to CDP’s climate change questionnaire. This analysis investigates the disclosing organizations’ alignment with TCFD recommendations and the reported financial impacts of climate-related risks and opportunities.

The Canadian Securities Administrators (CSA) proposed largely TCFD-aligned climate related disclosure requirements in October 2021. Furthermore, in its latest budget in April 2022, the Canadian government announced mandatory reporting of climate-related financial risks for all federally regulated financial institutions from 2024 (using a phased, ‘comply-or-explain’ approach). Financial institutions will be expected to report their climate-related risks in line with the TCFD recommendations. Analysing the existing state of S&P TSX Composite companies that disclose through CDP on TCFD indicators is important to provide a baseline to track progress in the coming years.

Key findings:

- The vast majority responded to at least 80% of TCFD-related questions in CDP's questionnaire, but only 12% responded against all indicators.

- Aggregated across the disclosing sample, the reported potential financial benefits of climate-related opportunities (US$517 billion) are significantly higher than the potential financial impacts of climate-related risks (US$18 billion).

- Unlike other indices analyzed within this series, market risks have the highest reported potential financial impacts, and market opportunities have the highest reported financial benefit.

- For most industries, taking action to respond to climate-related risks, and investing in realizing climate opportunities, comes at a lower cost (aggregated per industry) than allowing the risks to materialize or letting the opportunities go unrealized. The exceptions are the fossil fuel and power industries for both risks and opportunities, and the infrastructure industry for risks.

In 2021, 102 companies (85%) listed on the SBF 120 index, representing a market capitalization of over US$2.1 trillion, responded to CDP’s climate change questionnaire. This analysis investigates the disclosing organizations’ alignment with TCFD recommendations and the reported financial impacts of climate-related risks and opportunities.

Companies in this French stock market index will be required to provide TCFD aligned disclosures under the European Commission’s Corporate Sustainability Reporting Directive (CSRD). Furthermore, Article 29 of France’s 2019 Law on Climate and Energy sets a goal of achieving carbon neutrality by 2050, decreasing fossil energy consumption by 40% by 2030 and provides details on expected disclosures across both biodiversity and climate. It requires financial institutions to publish information on the portion of their assets complying with the environmental criteria set out in the EU Taxonomy. Companies providing TCFD aligned disclosures are well placed to meet these regulatory requirements.

Key findings:

- Over 93% of the companies responded to at least 80% of the TCFD-related questions in CDP's questionnaire, out of which only 18 companies responded to all of the TCFD indicators.

- Aggregated across the disclosing sample, the reported potential financial benefits of climate-related opportunities (US$479 billion) are about 6 times higher than the potential financial impacts of climate-related risks (US$131 billion).

- Acute physical risks were reported by the highest number of companies, but technology-related climate risks had the highest total financial impact (about US$50 billion reported by just 13 companies). The financial impact is driven by unsuccessful investments in new technologies, and substitution of existing products and services that are impacted by the transition to lower emissions options.

- For most industries, taking action to respond to climate-related risks, and investing in realizing climate opportunities, comes at a lower cost (aggregated per industry) than allowing the risks to materialize or letting the opportunities go unrealized. The exceptions are the materials industries for risks and the power industry for opportunities.

In 2021, 91 companies (66%) listed on the STOXX Germany Total Market index, representing a market capitalization of over US$1.9 trillion responded to CDP’s climate change questionnaire. This analysis investigates the disclosing organizations’ alignment with TCFD recommendations and the reported financial impacts of climate-related risks and opportunities.

All large companies meeting the mandate criteria will have to report under the European Commission’s Corporate Sustainability Reporting Directive (CSRD). The reporting requirements on a high level are aligned with the TCFD recommendations and TCFD aligned companies are already ahead of the regulatory curve.

Key findings:

- Over 75% responded to at least 80% of TCFD-related questions in CDP's questionnaire, but only 8% responded against all indicators.

- Aggregated across the disclosing sample, the reported potential financial benefits of climate-related opportunities (up to US$860 billion) are significantly higher than the potential financial impacts of climate-related risks (up to US$100 billion).

- Opportunities related to products and services were the most frequently reported, and 97% of the potential financial benefit of climate-related opportunities was reported in this category.

- For most industries, taking action to respond to climate-related risks, and investing in realizing climate opportunities, comes at a lower cost (aggregated per industry) than allowing the risks to materialize or letting the opportunities go unrealized.

In 2021, 32 companies (80%) listed on the FTSE MIB (Italian) index responded to CDP’s climate change questionnaire. This analysis investigates the disclosing organizations’ alignment with TCFD recommendations and the reported financial impacts of climate-related risks and opportunities.

The European Commission’s Corporate Sustainability Reporting Directive (CSRD) will come into force in 2024, bringing sustainability reporting to the same level as financial reporting. All large companies meeting the mandate criteria will have to report under the European Commission’s Corporate Sustainability Reporting Directive (CSRD). The reporting requirements on a high level are aligned with the TCFD recommendations and TCFD aligned companies are already ahead of the regulatory curve.

Key findings:

- With the exception of one company, all disclosers responded to at least 80% of the TCFD tagged questions, of which 6 companies (18.7% of the sample) have fully aligned disclosures.

- Aggregated across the disclosing sample, the reported potential financial benefits of climate-related opportunities (US$114 billion) are much higher than the potential financial impacts of climate-related risks (US$14.2 billion).

- The highest potential financial impacts of risks were associated with emerging regulations and highest financial benefits are associated with market related opportunities.

- For most industries, taking action to respond to climate-related risks and investing in realizing climate opportunities, comes at a lower cost (aggregated per industry) than allowing the risks to materialize or letting the opportunities go unrealized.